PREA Quarterly Feature - Winter 2023

Richard Kalvoda

Richard KalvodaAltus Group

Robby Tandjung

Robby TandjungAltus Group

Omar Eltorai

Omar EltoraiAltus Group

The year 2022 was challenging for investment assets. Carried on the momentum from 2021, the year started strong but stuttered as coordinated central bank actions across the globe, and most impactfully in the US, took aim at taming inflation. These central bank actions effectively raised the cost of capital across all sectors and geographies and forced a repricing of risk assets.

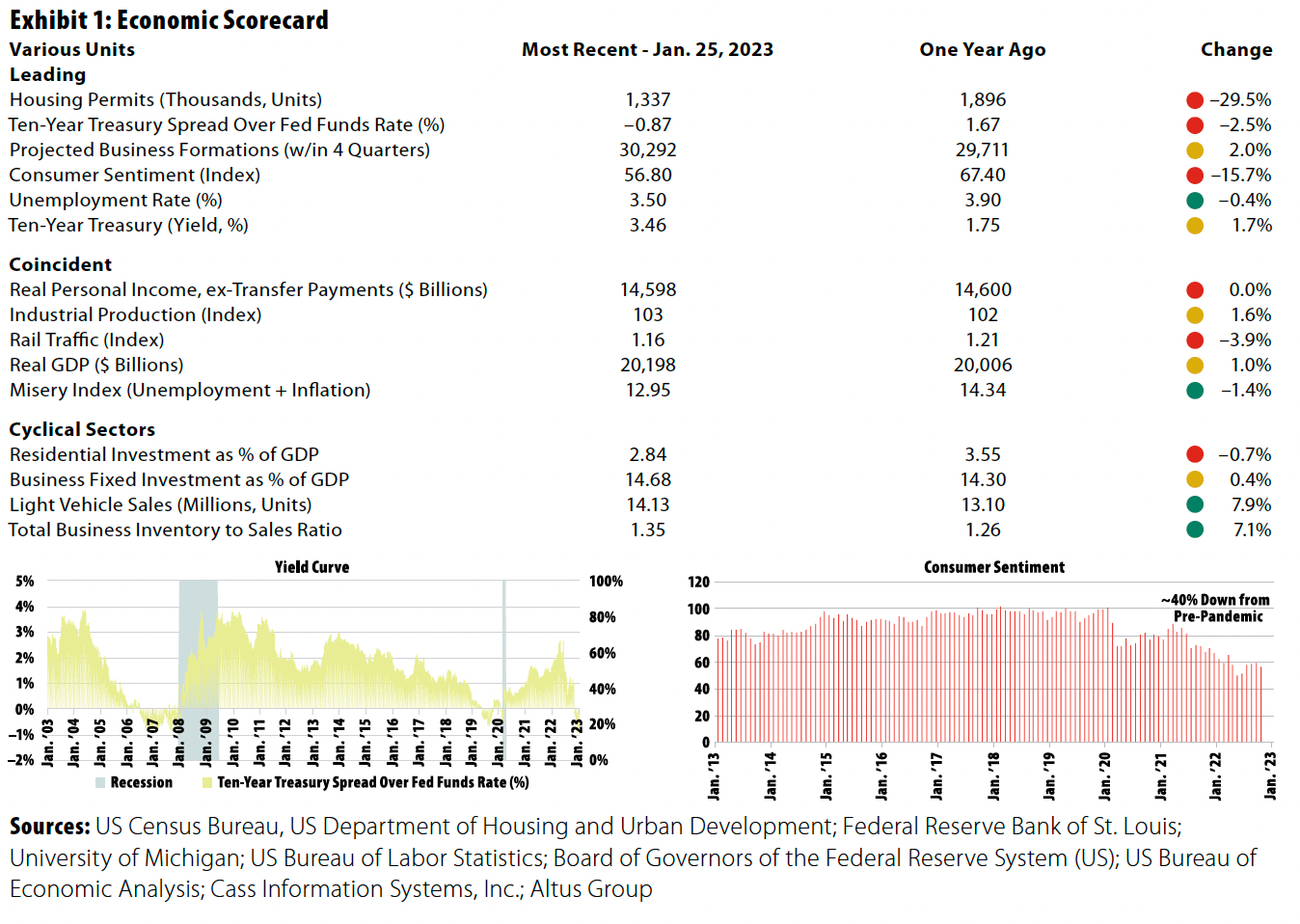

The immediate impact market participants felt in the second quarter of 2022 was a reversal of many of the trends that characterized the ebullient 2021 capital markets—a time of cheap money and a pandemic recovery. Despite many economic signals still showing strength, 2022 was soon marked by persistent inflation, aggressive central bank tightening, and a precautionary pullback by capital sources. As the year progressed, capital allocator and investor outlooks soured on lowered expectations for top-line growth caused by recessionary fears, margin pressure from higher costs of capital and higher operating expenses, and the thought of cresting profitability (Exhibit 1).

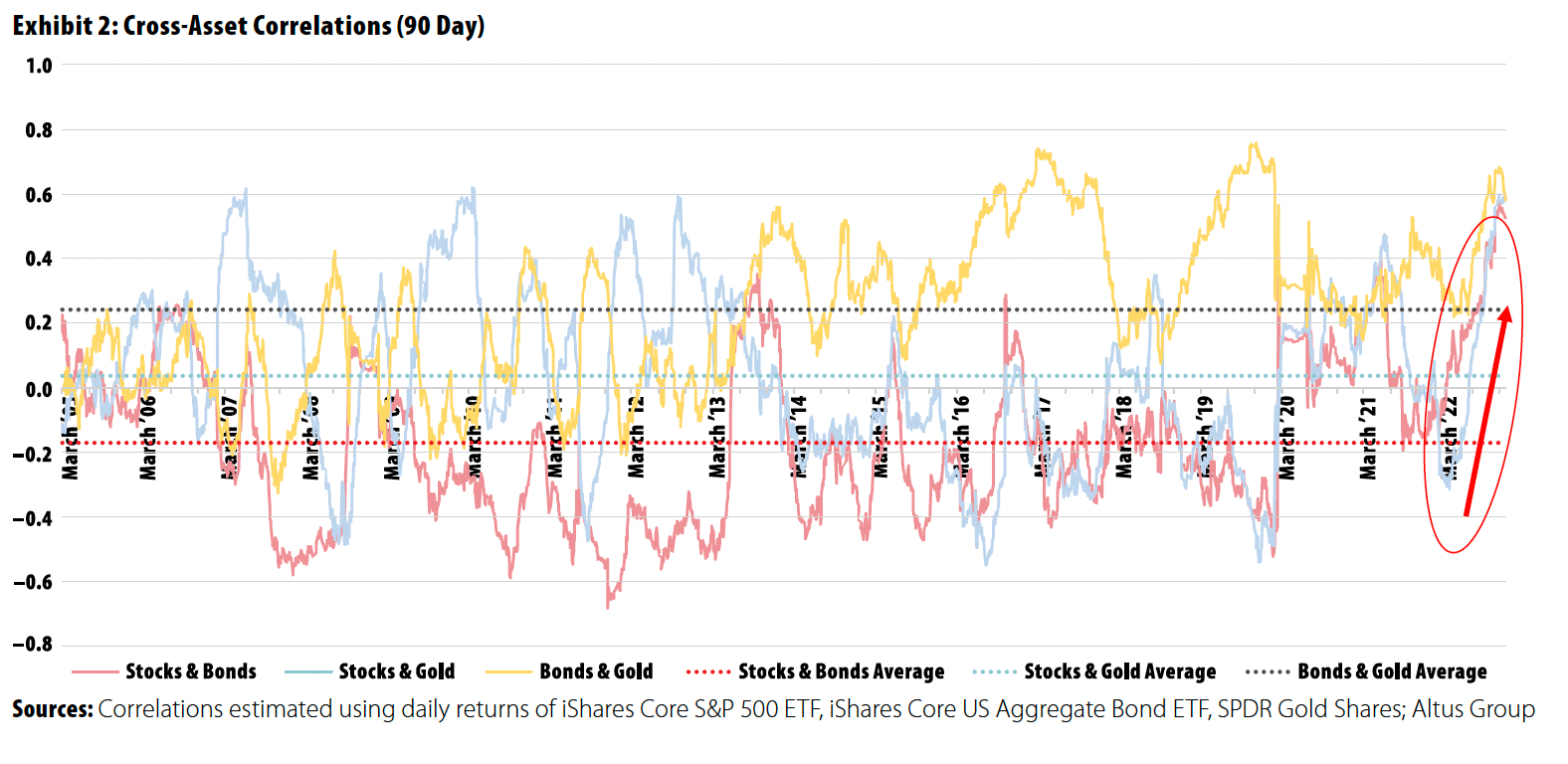

Across capital markets, liquid securities (e.g., stocks and bonds) sold off as growth expectations slid. The sell-off was so widespread that cross-asset correlations began to converge higher, as they often do during periods of public market anxiety (Exhibit 2). As public markets experienced falling prices, private market activity slowed as capital costs increased and capital availability declined. Many market participants began to call attention to the gap between public market and private market valuations as this public-private gap widened. Despite being an imperfect comparison (for reasons discussed in more detail below), the public-private gap is often watched because the two markets share similar exposures to underlying business fundamentals and generally move directionally together. The gap can contain some valuable information for market participants because of the similarities.

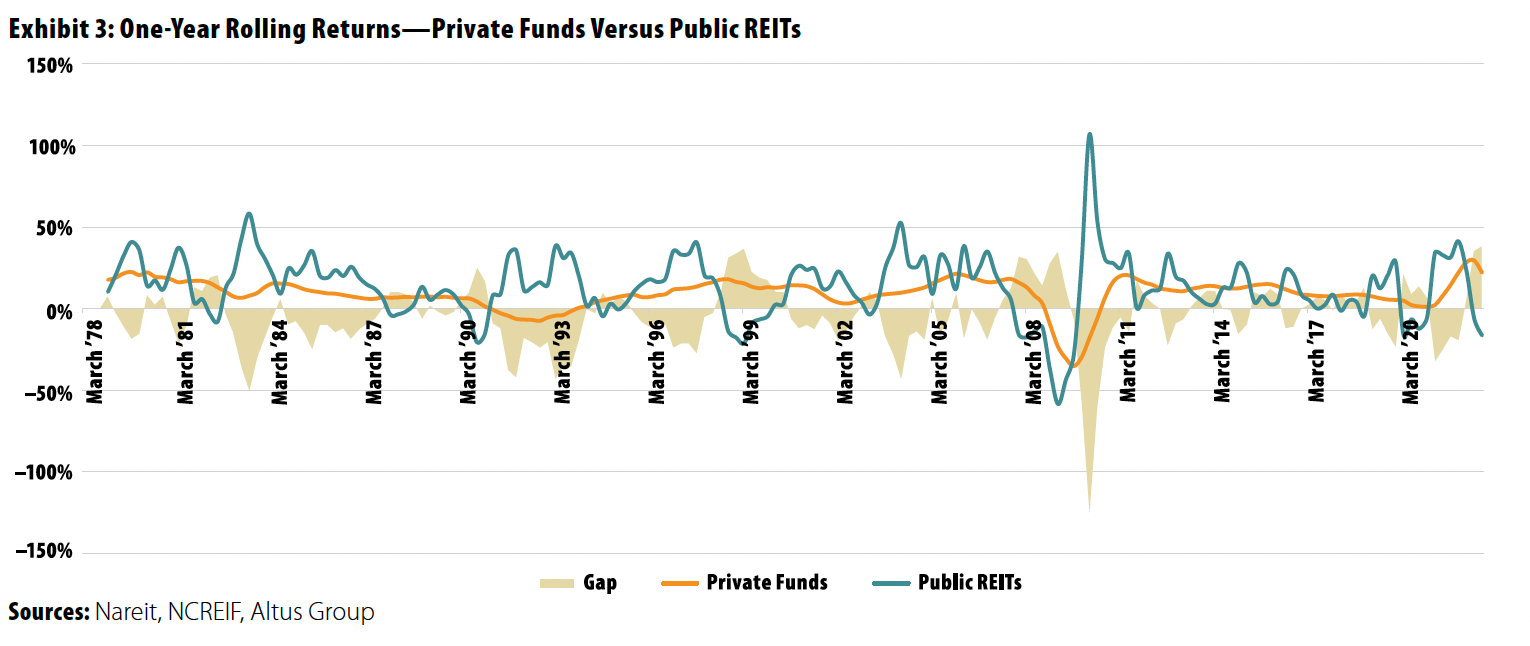

By the fourth quarter of 2022, the widening public-private gap was seen across nearly every sector, including commercial real estate (CRE). Market participants began tracking this public-private gap using indices of publicly traded shares of REITs and privately held open-end diversified core equity real estate funds. The broad equity market rout pulled REIT valuations down 25.1% for 2022, while private market valuations were up 7.4% on the year. This gap was 38.4% in 4Q2022, a notable and significant 2.1 standard deviation difference (Exhibit 3).

In the second half of 2022, as shares of public REITs fell, some private market fund investors (limited partners) took the widening public-private gap as a harbinger of lower future fund valuations and interpreted it as an opportunity to sell and exit their funds before the private fund values were marked down. Many media outlets picked up the story and took the angle that this was a sign of overvalued real estate assets in the private markets. And with this, the public market anxiety brought skepticism and criticism to the private markets.

The capital market developments over the past 12 months raised two pressing questions for CRE valuations:

- Are public market price movements relevant to private market valuations?

- Where are private market CRE valuations going in 2023?

CRE Appraisals

Commercial real estate appraisals are an essential tool used to determine the value of a property or portfolio of properties. The appraisal process involves comprehensively analyzing a property’s physical attributes, location, and market conditions to arrive at a fair market value.

The definition of “market value” in the context of commercial property appraisals in the US refers to the estimated price at which a property would be sold in an open and competitive market between a willing buyer and a willing seller, both of whom are knowledgeable and motivated. A measure of the property’s worth, the appraised value takes into account a property’s location, physical characteristics, and current market conditions.

The assumptions underpinning market value mean that it is a dynamic concept that can change over time because of changes in market and property conditions. In commercial real estate appraisals, the appraiser’s objective is to estimate the property’s market value as of a specific date. To do so, the appraiser utilizes factual historical and current data provided by the owner to inform the valuation. The appraisal considers multiple valuation approaches and detailed analysis of the market, property, competition, and financial conditions before arriving at the concluded value. Values tend to rely most heavily on a discounted cash flow approach, which is then supported by a comparable sales approach. In this way, valuations are able to be done consistently, even when no recent comparable transactions are available.

The appraisal process combines a consistent and detailed methodology to ensure consistency of approach. Although the independent appraiser performs the appraisal, multiple parties in the process (appraiser, appraisal reviewer, investment manager, asset manager, accountants, etc.) ultimately review and sign off on the final appraisal report and objective market value.

Are Public Market Price Movements Relevant to Private Market Valuations?

Yes, but not significantly. Both public market REITs and private market CRE funds derive their value from cash flows generated by commercial real estate, so both can have similar exposures to underlying operating fundamentals. Both tend to take ownership stakes in commercial real estate properties to generate a return to shareholders. Additionally, both are institutionally managed for financial purposes, so both have competent, return-oriented management teams. Finally, given the overlap and shared functions, public REITs and private CRE funds can and will often compete.

That’s about where the similarities end.

Not Quite Apples to Apples

The list of differences between public REITs and private CRE funds exceeds that of similarities. Notable differences include these:

- Exposure: Private CRE funds allow investors exposure to return and risk via direct investment in real estate. In contrast, REITs (among other security types, including mutual funds and exchange-traded funds) offer indirect investment exposure. Generally, direct investments offer more control to the management company (e.g., fund manager, general partner) but often also require more time and resources and less liquidity. On the other hand, indirect investments tend to provide greater liquidity and diversification but with less control.

- Size and Market Share: We estimate more than $18.8 trillion worth of CRE value is across 3.8 million properties in the US market. In aggregate, private CRE funds own 431,000 properties (11.2% total count), worth an estimated $2.0 trillion (10.8% total worth), and REITs own 67,100 properties (1.7% total count) worth an estimated $329 billion (1.7% total worth). In other words, although institutional managers (private CRE funds and REITs) hold approximately 12% to 13% (12.9% of properties and 12.6% of total value), the aggregate ownership of private CRE funds is nearly eight times that of REITs. Though trends seen across REIT portfolios may be indicative of broader market and operating trends, even in aggregate, REITs are a minority of the larger CRE market (Exhibit 4).

- Structural: Although REIT structures have multiple variations (public, public nontraded, private), the public-private gap focuses predominantly on the public REIT variations. These public REITs are companies that own and operate income-generating real estate assets. The legal entity structure of REITs allows for certain favorable tax treatment for the REIT entity and its investors. Still, the tax benefit comes with less flexibility at the entity level, including dictating distributions of income and certain ownership requirements. On the other hand, private equity real estate fund entities may have fewer tax benefits but significantly more flexibility in terms of entity structure and cash flow distributions. The different legal structures also affect how the shares can be marketed to potential investors and reporting requirements.

- Investors: The structural differences between REITs and private CRE funds influence the types of investors each type attracts. Given the bespoke ownership structure and longer investment periods, private CRE funds’ shares are less accessible and liquid. As a result, most private CRE fund investors are large institutional and accredited investors. In contrast, public REITs tend to have a greater degree of both investor access and liquidity. Listed on stock exchanges, many public REITs have similar ownership share structures, allowing investors of all sizes (institutional and retail/nonaccredited investors) to buy and sell.

- Holding Periods: Share liquidity and access affect the typical holding periods for investors in each investment type. Estimating the average holding period, implied by turnover ratios, for investors in public REITs and private CRE funds is complicated by differences in time horizons, lockup or commitment periods, and a lack of share transaction data. However, a rough estimate using turnover ratios suggests that investors in public REITs hold their shares for about half the time (47% less) as investors in private CRE funds.

- Transparency: Data is critical to managers at both public REITs and private CRE funds; they use it to make decisions, monitor their portfolios, identify opportunities, and report to stakeholders. However, one significant difference between public REITs and private CRE funds is the degree of information they make available externally. Public REITs are subject to the reporting and data requirements that all publicly traded companies are subject to, and tools exist to efficiently aggregate this data across all REITs, allowing for rapid and thorough analysis of REIT shares. Private CRE funds have many reporting requirements, but the aggregation of the data across the private CRE fund space is less centralized, requiring more time and involving more stakeholders. The result is that at the REIT or private fund level (not asset level), public REITs provide higher frequency and more comparable data externally than private funds. Because there is more transparency when it comes to price discovery of REIT shares, it is tempting to make the assumption that REIT share price movement reflects the market values of the individual properties REITs held. However, this logical extension is flawed. Public market REITs do provide greater transparency about share prices, but the pricing does not reflect the underlying property values.

- Pricing and Valuation: At the crux of the public-private gap conversation is the issue of “price versus value.” The reason this is the core issue is because any comparison relies on prices for the public REITs and values (net asset values, or NAV) for the private CRE funds. Like stocks, the price of public REIT shares is based on the last trade executed during trading hours. Private CRE funds are valued periodically (usually monthly or quarterly) based on net asset values, which are the appraised values of the assets less liabilities and capital expenditures. Though prices and values do trend together, they are fundamentally different concepts.

Minding the Public-Private Gap

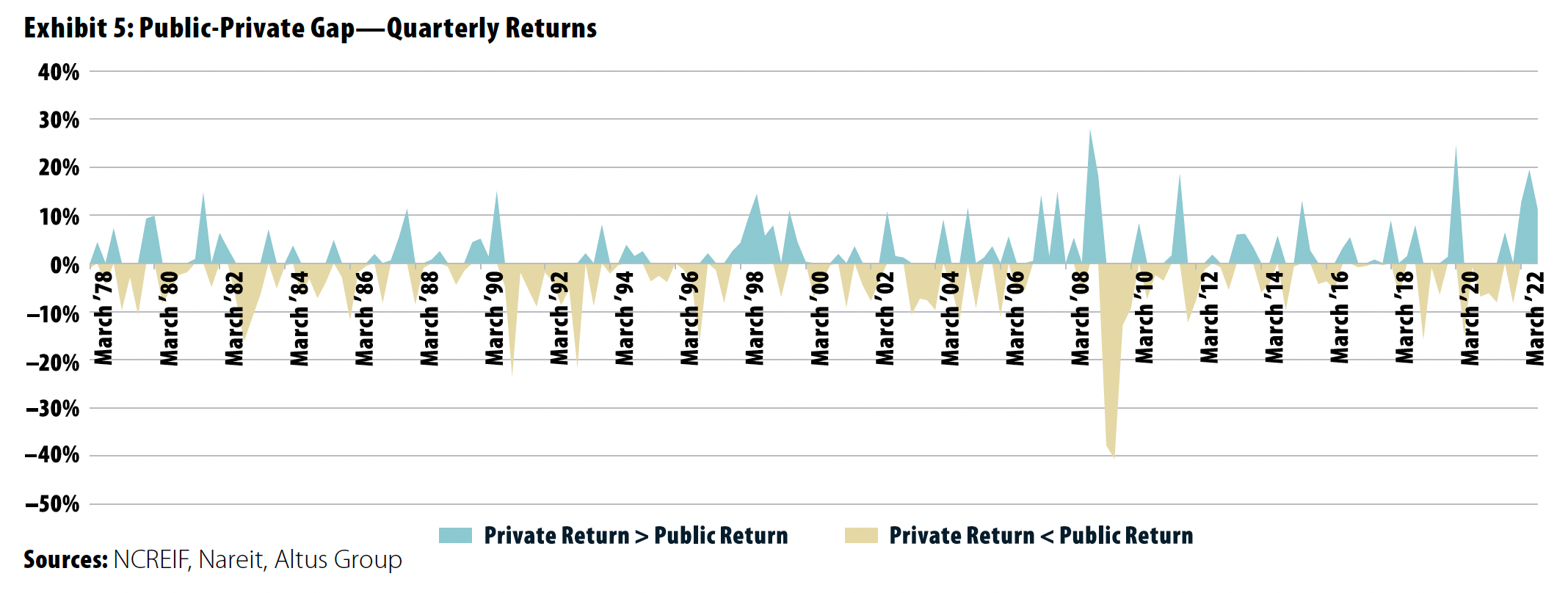

With the differences noted above, it is little surprise that a public-private gap exists. Since 1978, the gap between one-year rolling returns for public REITs and for private CRE funds has exceeded +/–500 basis points (bps) 80% of the time. Quarterly returns have differed between the two investment types by +/–500 bps 53% of the time (Exhibit 5).

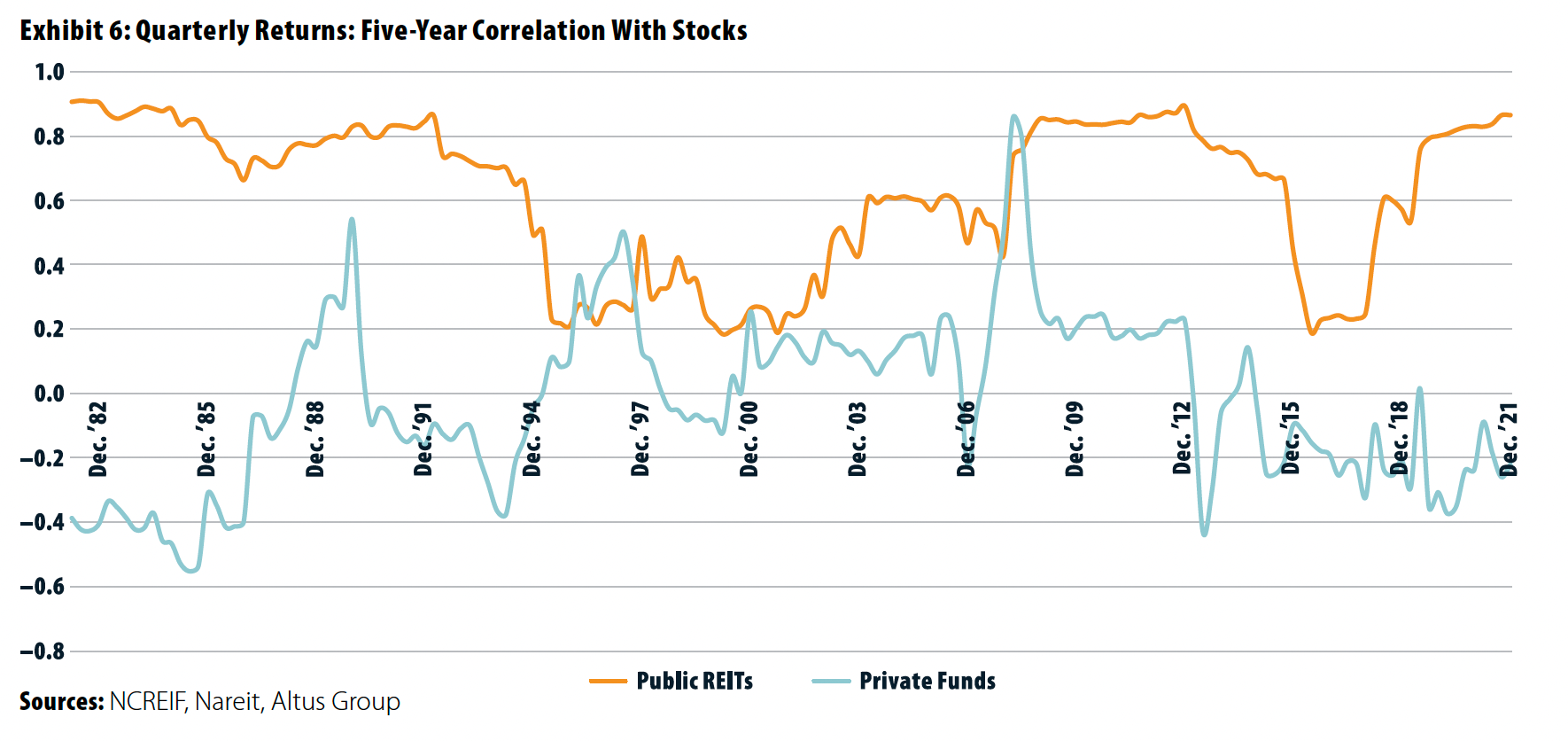

One key reason this gap persists is because public REIT prices move significantly more than private CRE fund NAVs. Over the past 44 years, the standard deviation of quarter-end public REIT prices was 8.9%, more than three times private CRE funds’ 2.7%. This volatility may be partially explained by the correlation of public REIT prices with the broader stock market. The long-term rolling five-year correlation of quarterly returns for the broad stock market and public REITs has averaged 0.6 (R-squared:0.45) but climbed to more than 0.8 in the most recent quarters. Meanwhile, the same rolling five-year correlation of quarterly returns for stocks and private CRE funds has averaged 0.0 (R-squared:0.0) but recently sits near –0.2 (Exhibit 6).

The similarities between public REIT price movements and the broader stock market movements are further illustrated by public REIT share price movements compared to estimates of the same REITs’ NAVs. Over the past two decades, public REIT shares have differed from their NAVs by +/–500 bps nearly two-thirds of the time, approximately 63%. (Obviously, a similar price-to-NAV comparison for private CRE funds is not possible.)

To quickly recap the key points:

- The public-private gap is not a new phenomenon and has existed (+/–500 bps) nearly 80% of the time dating back more than four decades.

- The gap is largely caused by public REIT price swings, which are more than three times more volatile than private CRE fund NAVs.

- The public REIT price swings appear to be more closely related to the broader stock market than to private CRE fund NAVs.

Where Are Private Market CRE Valuations Going in 2023?

Many questions were raised in 2022 and few have answers. We think 2023 will likely provide some clarity. Although valuations may be tested as macro developments dominate the news cycle, CRE as an asset class continues to have a number of mitigating factors to help it weather any rough conditions:

- In aggregate, CRE continues to have relatively strong fundamentals compared to those of prior downturns.

- Lenders and developers have had greater discipline compared to prior cycles.

- Inflation has generally benefited the asset class.

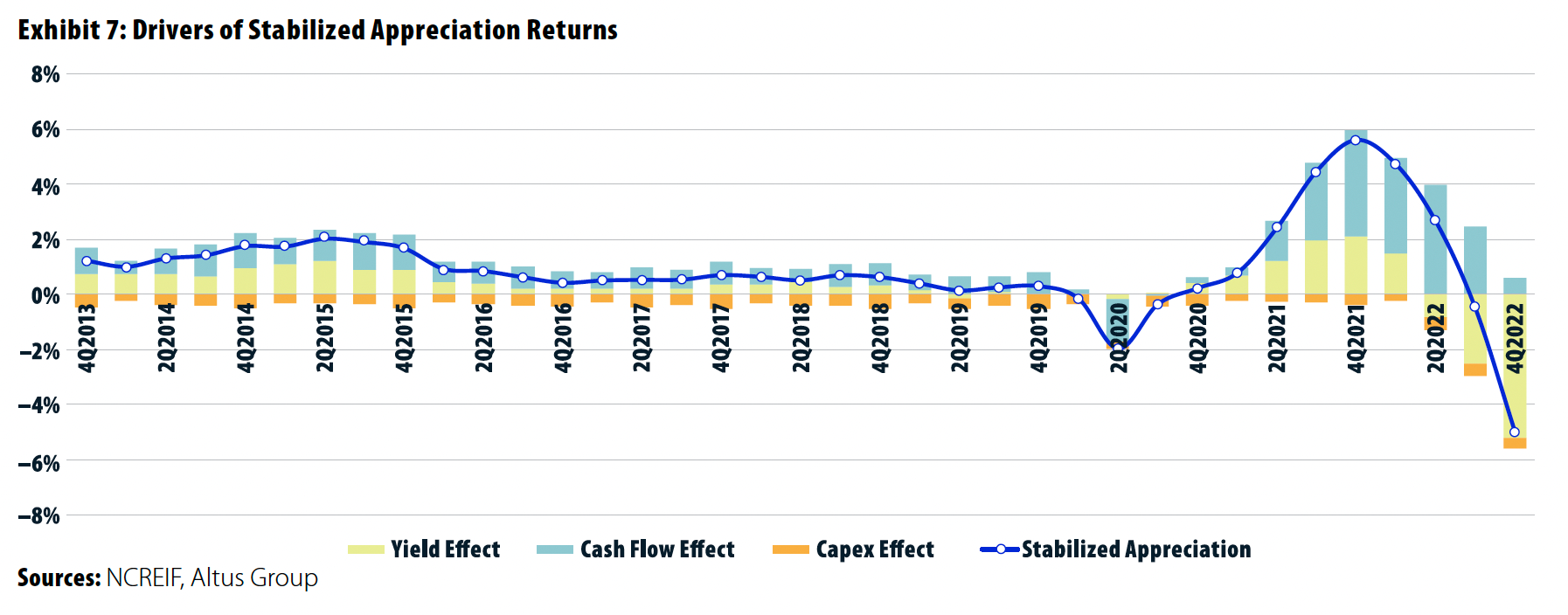

The most recent private fund data from the fourth quarter of 2022 shows some of this testing of values is already underway. Although the shifting cap rates have had the largest negative effect on returns recently, the cash flow effect has deteriorated rapidly from its post-pandemic high and is now in range of (and slightly below) pre-pandemic levels (Exhibit 7).

Where Is the Capital? What’s the Cost?

As the Fed aggressively hiked interest rates in 2022, the higher costs of capital were transmitted through the financial system and across capital markets. Higher capital costs combined with slower growth expectations and recessionary concerns caused many lenders to tighten underwriting standards and decrease availability of capital. Coming into 2023, nearly three-fourths of bank lenders reported tightening underwriting standards for CRE loans. The combination of higher rates and tighter underwriting helps explain the precipitous decline in demand for debt capital (Exhibit 8). The rapid decline in bank-reported demand fell at a rate not seen since the pandemic began.

Although the debt markets will remain challenged through 2023, the emergence of alternative, non-bank lenders and a partial thawing of CMBS markets will likely be able to selectively accommodate the top performers, but the debt markets will also remain well below 2021 levels in terms of new originations. As a result of the cautious and costly debt capital markets, transaction activity may remain challenged throughout the year. This scenario could change, though, if debt capital becomes more accessible; even if at a higher rate, availability is the key driver for transaction activity in 2023.

Will Macro Matter More Than Market?

Macro events will continue to play a major role in 2023, but local market factors will matter more for investment performance. Because of a slowing population growth rate, an increasing portion of “seasoned” (elderly) citizens, and the widespread adoption of remote work (even if only a few days per week), local market selection will become more critical because of fewer but more mobile populaces. These demographic and labor shifts will be key drivers in determining which markets are over- and under-supplied and will play a major role in driving the outperformance and underperformance of assets.

2023 to Bring Bumps, Not Breaks

Despite looking as if 2023 will be a bit bumpy for CRE, the asset class will prove its staying power. With downward pressure on cash flows and higher cap rates, private market CRE valuations will likely pare gains from the past two years, though not to the same extent that public REIT prices fell during 2022. Unlike the pandemic recession, the next recession will likely look more like a “traditional” recession for both public and private markets, characterized by somewhat overreactive public markets and a scarcity of private market transactions, of which a larger portion is distressed. And though the recessionary period will look familiar, it is unlikely to be similar to the global financial crisis. CRE as an asset class will continue to attract capital, though asset selection will be paramount as the performance of the asset class becomes much more nuanced.

Richard Kalvoda is the President of Altus Analytics–Americas, Robby Tandjung is Global Head of Business Advisory Services, and Omar Eltorai is Director of the Research Team at the Altus Group.

This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes a available or circumstances existing or changes occurring after the date the article was prepared.